By Lenka Moore, Capitals Coalition

The financial world is moving away from considering nature finance as conservation-focused, low-return vehicle dependent on public or philanthropic capital. Financial institutions are increasing their awareness of the risks nature loss poses to their loans, investments or underwriting and are no longer waiting to take action. Some are starting to explore the opportunities that investing in nature and resilience presents – not as a standalone isolated “green” action, but rather as a core strategy based on informed understanding of nature risks in their portfolio and direct capital towards nature-aware and / or positive opportunities. Complexity remains, but mainstream finance (banks, investors and insurers) is beginning to make nature-aware decisions, going beyond the exploratory and incremental steps to embed nature considerations into their strategies and decision-making.

Nature loss is a financial risk

While the WEF estimates that over half of global GDP depends on nature, the reality is that 100% of our economy and society relies on a healthy natural system as all companies and humans depend on nature. This increased understanding is being translated by governments and the public sphere more generally into international policies and agreements such as the Global Biodiversity Framework, and, in 2024, the Nature-related financial risks to guide actions of Central Banks and Supervisors framework published by the Network for Greening Financial System (NGFS). The framework is a clear signal not just to central banks, but also the financial institutions they supervise: nature loss translates into traditional financial and economic risks through for example, water stress, deforestation, climate change, decline and degradation of ecosystems affecting supply chains leading to reduced profitability, stranded assets, defaults on loans on or even areas that are no longer insurable.

And yet, UNEP’s latest State of Finance for Nature 2026 report shows that for every US dollar invested in protecting nature, 30 US dollars are spent destroying it. The report also highlights that, to meet global biodiversity, climate and land restoration targets, investment into nature must increase 2.5 times to US$571 billion annually by 2030. This is the equivalent of just 0.5 per cent of global GDP. The good news is that there are actions that financial institutions can already take today to realign mainstream finance flows towards reducing harm to nature and also towards nature-positive outcomes. This Scaling Finance for Nature: a primer on what financial institutions are doing today highlights some of those actions that banks, insurance companies and investors are taking to demonstrate that action is possible today and hence serve as an inspiration for others.

Practical actions done by financial institutions today

Financial institutions have a profound influence on the real economy through the way they allocate financial capital to companies and projects. They can act for nature by reducing their financing of activities that harm nature, advocating for change within their existing investment, underwriting or lending portfolios and by increasing finance for activities that contribute to nature’s protection and restoration. These actions can be embedded in existing financial processes (e.g. portfolio construction, risk management), and via traditional products, services, investment structures and asset classes.

The first fundamental step for financial institutions is to understand their impacts and dependencies on nature through the companies and projects they finance. There are a number of guides (e.g. Why nature loss is material for your financial institution) , frameworks such as TNFD’s LEAP Approach or Natural Capital Protocol and tools such as the ENCORE (Exploring Natural Capital Opportunities, Risks and Exposure) or the recently released Nature Tools Compass that will help financial institutions and businesses to navigate through 70+ tools available to assess their nature-related dependencies, impacts, risks and opportunities.

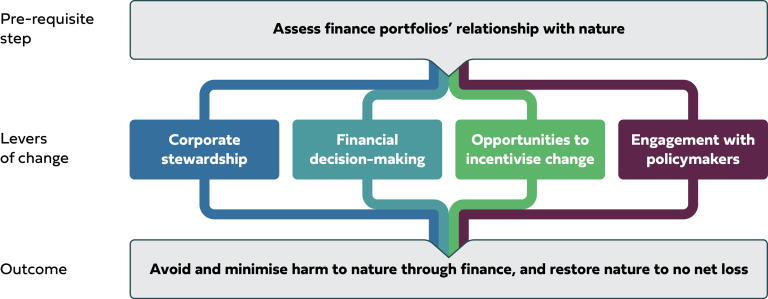

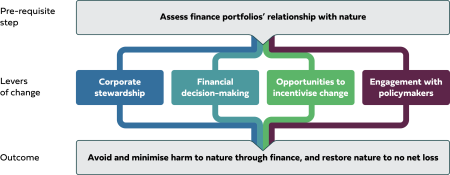

After understanding their dependencies and impacts, financial institutions have four key levers of change available to scale up their action on nature.

Lever 1: Corporate stewardship – encouraging businesses to reduce their negative impacts on nature and/or increase their positive ones is often the first key lever used by financial institutions. Examples include activities such as dialogue with companies on key topics such as deforestation, biodiversity, water and land use, establishing behavioural expectations along with timebound milestones for improvement, filing shareholder resolutions, voting and imposing conditions prior to investment.

Lever 2: Financial decision-making lever is informed by better knowledge of a portfolio’s relationship with nature and embeds nature considerations across day to day working practices. It usually involves development of internal policies to address and incorporate nature-related issues. Actions could include understanding nature-related tools and metrics, implementing restrictions based on geographic location and highly polluting substances and developing own benchmarks.

Lever 3: Opportunities to incentivise change. This lever is about making more finance available and using financing terms to incentivise positive change in companies receiving capital. Some of the actions used by financial institutions are ensuring that existing financial products are available to activities and companies that are shifting the balance towards nature positive; offering preferential terms for nature-positive activities; and making sure that incentives for key decision-makers, such as executive management, are aligned with a strategy for improved nature outcomes. Such opportunities can significantly scale up finance for nature.

Lever 4: Engage with policymakers. The financial sector can advocate for positive change in public policy and standard-setting bodies, both nationally and internationally. For example, a collaboration between financial institutions can amplify calls for government policies that support long-term environmental and positive business goals – such as promoting nature-positive investments and ending harmful subsidies.

Scaling can happen through mainstream finance

Nature finance has often been considered niche, philanthropic and/or scaleable only through special funds. However, nature loss is increasingly considered financially material amongst financial institutions as well. As Norges Bank Investment Management (NBIM), an institution that manages Norway’s sovereign wealth fund worth over $2 trillion USD, said, “[the] degradation of land, freshwater systems, and marine environments all affect the long-term value of companies in our portfolio” and that nature degradation already affects their portfolio. NBIM just set out clear nature expectations for boards of the companies it invests in - setting a leading example to others in the market.

This A-Track primer helps financial institutions on their nature by highlighting a variety of actions implemented by banks, investors and insurers who are already embedding nature into mainstream markets as part of everyday loans, insurance, investments and stewardship decisions. The financial institutions that integrate nature-related risks and opportunities into their decision-making, investment analysis and risk management are much better positioned for evolving and increasing regulations and expectations from customers in the face of more unpredictable availability of natural resources.